Hormuz Under Fire, Capital Rotates Elsewhere

As missiles strike tankers and Washington rewrites the security bargain, the Gulf's strategic premium is being repriced in real time — and IOC capital is voting with its feet.

The Gulf's implicit security guarantee — the invisible subsidy underwriting four decades of MENA hydrocarbon dominance — is being renegotiated at gunpoint, and the capital allocation consequences are already visible.

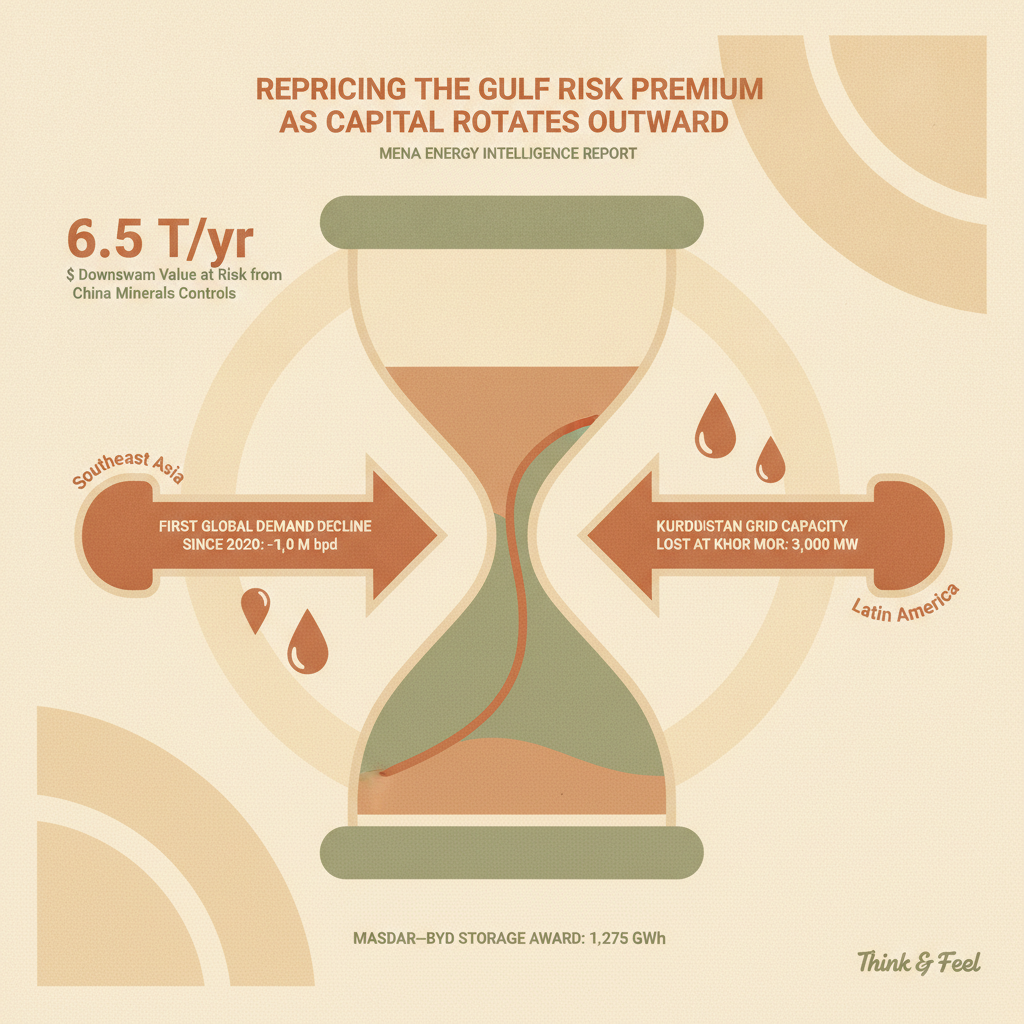

This week's dominant signal is not a barrel count or an EPCI award — it is a repricing of Gulf risk. The UAE's accusation that Iranian missiles struck tankers inside the Strait of Hormuz (Reuters), combined with renewed US strikes and a naval blockade of Iranian ports (The Guardian), has pushed the IEA to forecast the first annual global oil demand decline since 2020. The strategic question for MENA capitals is no longer how to defend the chokepoint, but how to build around it.

Macro Layer

The IEA now projects global oil demand to contract by roughly 1 million bpd in 2026, with OPEC quietly following with its third consecutive downward revision to 780,000 bpd of growth (OilPrice). That forecast is itself conditional on a gradual Hormuz reopening the market cannot yet verify. Prices firmed on the week as US–Iran tensions intensified (Rigzone), but the risk premium is now structural rather than episodic. Layered on top, Donald Trump's suggestion that Gulf states should pay directly for US protection of the Strait (The Hill) reframes the security relationship as transactional — a shift that will echo through sovereign defense budgets from Riyadh to Abu Dhabi. CNBC's reminder that bypass pipelines mitigate but never fully neutralize Hormuz risk reinforces the point: redundancy is not resilience. And beyond hydrocarbons, the IEA's Critical Minerals Outlook warns that Chinese export controls could put $6.5 trillion of downstream production at risk — a supply-chain fragility that directly threatens the industrial diversification and decarbonization playbooks underpinning Vision 2030 and the UAE's Net Zero 2050.

Execution Layer

Even as macro sentiment sours, execution capital is being deployed selectively — and increasingly outside the Gulf. Eni CEO Claudio Descalzi told an Italian parliamentary committee that majors are rotating upstream capex toward Southeast Asia and Latin America, citing Hormuz disruption as a permanent risk premium (OilPrice). Eni's Searah JV with PETRONAS consolidates 19 upstream gas assets across Indonesia and Malaysia, while Eni and Abu Dhabi's XRG are co-developing the ~$30 billion Argentina LNG complex — a telling hedge by an Emirati vehicle against its own home-basin exposure. Chevron, Repsol and Eni are simultaneously scaling Venezuelan heavy crude, though Rystad flags a critical oilfield services bottleneck: 93 active rigs required by 2028 against current mobilization capacity. That rig-market tightening will spill into GCC service pricing. On the transition side, Masdar's award to BYD for an 11.275 GWh battery storage system (TaiyangNews) — one of the largest BESS contracts globally — anchors the UAE's grid-firming strategy and demonstrates that renewables EPCI momentum is decoupling cleanly from oil-market volatility. Meanwhile, SLB and Liberty Oilfield Services announced an alliance to build data center capacity (Rigzone), signaling that oilfield service majors now see AI infrastructure as an adjacent power-hungry vertical — a thesis with immediate GCC application.

Company Moves

The week's sharpest company-level signal comes from Iraq's Kurdistan Region, where Dana Gas has suspended all main production at Khor Mor following credible security threats — cutting more than 80% of the KRG's electricity supply and stripping up to 3,000 MW from the grid (OilPrice). The Pearl Petroleum consortium — Dana Gas and Crescent at 35% each, with OMV, MOL and DNO splitting the balance — had just commissioned the $1.1 billion KM250 expansion, lifting capacity to 750 MMSCFD. The contradiction is stark: a field engineered to reduce Baghdad's dependence on Iranian gas is now offline precisely because of Iran-adjacent security dynamics. In Egypt, BP has guided lower upstream production for Q2 2026 (Egypt Oil & Gas), a headwind for Cairo's already fragile gas balance and LNG export ambitions — and a reminder that IOC portfolio prioritization is quietly reshaping East Med supply. In global LNG, Energy Intelligence reports West African cargoes swinging from Europe to Asia on premium spot pricing, which sharpens direct competition for QatarEnergy, Sonatrach and EGAS across both basins. Finally, Chevron's continued positioning around Iraq's largest oil prize is being framed explicitly as a Hormuz exit strategy — a phrase that would have been unthinkable a year ago.

What to Watch

Three signals will define the next fortnight. First, whether Hormuz tanker traffic stabilizes or degrades further — the IEA's entire 2026 balance is hostage to that single variable. Second, GCC sovereign responses to Washington's transactional security framing: expect accelerated defense procurement announcements and quiet diversification of security partnerships. Third, watch for follow-on BESS and grid-scale storage awards across Saudi Arabia and Oman on the Masdar–BYD template. If IOC capex rotation hardens into a multi-year trend, the ICV and Saudization frameworks will need to work harder — because the marginal upstream dollar is increasingly landing in Georgetown, not Ghawar.